'%3e%3cpath%20id='Path_84134'%20data-name='Path%2084134'%20d='M463.506,45.319c.05.9.033,1.834,0,2.733-1.366,37.226-54.177,81.06-91.112,74.809-10.2-1.727-25.263-14.509-28.533-24.267-15.13,5.322-37.38,18.858-48.975,1.253-12.431,4.049-23.175,12.207-36.808,6.808-20.683-8.185-3.374-45.768-11.014-51.912-2.3-1.854-8.933-1.069-10.547,1.039-2.242,2.926-6.341,21.882-8.85,27.765-3.571,8.359-13.353,25.463-23.472,25.891-15.541.655-21.848-26.856-28.537-27-5.432-.117-17.813,29.362-23.435,28.376L134.186,80.861c-2.953.01-18.631,26.612-25.052,28.436C98.42,112.344,96,96.145,90.188,90.426c-32.439,42.695-68.161,11.245-52.994-34.914,7.583-23.078,26.539-38.048,51.5-34.664,21.407,2.9,22.66,29.515,1.617,27.1-8.853-1.016-12.491-7.517-21.5.728-5.876,5.379-18.314,32.552-6.047,33.594,12.11-1.8,18.073-30.407,32.215-23.94,4.3,1.968,10.122,15.528,14.97,12.755,3.869-5.435,22.009-30.661,27.037-31.249,8.141-.949,14.342,17.956,19.223,23.242,4.149.986,15.387-27.538,25.42-22.587,5.051,2.492,17.823,34.667,22.67,33.514l8.9-19.871c-.184-3.531-7.266-5.315-8.913-11.509-4.657-17.522,11-29.482,25.954-20.322,3.384,2.071,5.365,7.109,7.306,7.771,7.914,2.686,26.789-3.448,33.534,3.568,6.688,6.959,1.417,31.867,2.612,42.481.187,1.65.217,4.149,2.232,4.634,1.824.441,12.615-4.6,13.657-6.742,3.832-7.884-3.464-37.219,5.659-43.553,7.163-4.968,17.475-3.885,20.773,4.978,2.84,7.644.334,9.575.311,15.975-.02,4.41-.722,26.435,1.607,27.892,5.245.611,13.54-.668,13.647-7.283.124-7.35-2.218-15.9-1.42-24.631C332.382,22.97,351.861,5.8,376.573,13.519c3.762,1.173,10.764,5.756,13.37,5.746,4.75-.017,18.494-8.389,27.668-9.294,22.346-2.2,44.569,11.405,45.9,35.348m-92.128-5.472c-30.514-.9-8.622,59.9,11.014,56.829,15.3-2.4,49.273-25.279,51.912-41.445,1.416-8.679-1.771-15.464-11.355-15.494-17.118-.05-48.391,37.52-51.571.11'%20transform='translate(78.646%2022.796)'%20fill='%231c63b7'/%3e%3cpath%20id='Path_84135'%20data-name='Path%2084135'%20d='M4.982,97.261c6.2-6.448,22.988-7.908,26.125,2.492,2.432,8.055-2.148,13.4,9.4,16.617,13.3,3.7,45.481-9.528,38.946-23.642C72.111,76.873.709,78.864,3.235,43.041,5.62,9.193,78.194-9.863,104.242,5.241c18.765,10.881,9.01,34.881-7.677,29.485-4.644-1.5-8.93-8.312-14.946-9.742-10.694-2.542-25.767.965-35.4,6.01-8.506,4.453-17.556,11.429-5.529,18.26,17.429,9.9,61.693,13.9,65.5,37.383,7.413,45.741-62.679,68.529-94.677,44.879-10.323-7.63-16.343-24.05-6.528-34.256'%20transform='translate(-0.001%200.002)'%20fill='%231c63b7'/%3e%3cpath%20id='Path_84136'%20data-name='Path%2084136'%20d='M122.432,4.842C146.756.426,150.8,31.288,128.615,34.3c-20.993,2.85-26.235-25.814-6.184-29.455'%20transform='translate(257.1%2010.325)'%20fill='%231c63b7'/%3e%3c/g%3e%3c/svg%3e)

'%20fill='%231c63b7'/%3e%3c/clipPath%3e%3c/defs%3e%3cg%20id='Group_820'%20data-name='Group%20820'%20transform='translate(0%200)'%3e%3cg%20id='Group_819'%20data-name='Group%20819'%20clip-path='url(%23clip-path)'%3e%3cpath%20id='Path_28'%20data-name='Path%2028'%20d='M162.285,20.389c.015.268.01.549,0,.818-.409,11.143-16.217,24.264-27.273,22.393-3.053-.517-7.562-4.343-8.541-7.264-4.529,1.593-11.189,5.645-14.66.375-3.721,1.212-6.937,3.654-11.018,2.038-6.191-2.45-1.01-13.7-3.3-15.539a3.018,3.018,0,0,0-3.157.311c-.671.876-1.9,6.55-2.649,8.311-1.069,2.5-4,7.622-7.026,7.75-4.652.2-6.54-8.039-8.542-8.081-1.626-.035-5.332,8.789-7.015,8.494l-5.4-8.967c-.884,0-5.577,7.966-7.5,8.512-3.207.912-3.93-3.937-5.671-5.649-9.71,12.78-20.4,3.366-15.863-10.451,2.27-6.908,7.944-11.389,15.415-10.376,6.408.869,6.783,8.835.484,8.111-2.65-.3-3.739-2.25-6.436.218-1.759,1.61-5.482,9.744-1.81,10.056,3.625-.539,5.41-9.1,9.643-7.166,1.286.589,3.03,4.648,4.481,3.818,1.158-1.627,6.588-9.178,8.093-9.354,2.437-.284,4.293,5.375,5.754,6.957,1.242.3,4.606-8.243,7.609-6.761,1.512.746,5.335,10.377,6.786,10.032l2.663-5.948c-.055-1.057-2.175-1.591-2.668-3.445-1.394-5.245,3.292-8.825,7.769-6.083,1.013.62,1.606,2.128,2.187,2.326,2.369.8,8.019-1.032,10.038,1.068,2,2.083.424,9.539.782,12.716.056.494.065,1.242.668,1.387.546.132,3.776-1.376,4.088-2.018,1.147-2.36-1.037-11.141,1.694-13.037,2.144-1.487,5.231-1.163,6.218,1.49.85,2.288.1,2.866.093,4.782-.006,1.32-.216,7.913.481,8.349,1.57.183,4.053-.2,4.085-2.18.037-2.2-.664-4.76-.425-7.373.668-7.31,6.5-12.45,13.9-10.139,1.126.351,3.222,1.723,4,1.72,1.422-.005,5.536-2.511,8.282-2.782,6.689-.66,13.341,3.414,13.738,10.581m-27.577-1.638c-9.134-.27-2.581,17.931,3.3,17.011,4.581-.717,14.749-7.567,15.539-12.406.424-2.6-.53-4.629-3.4-4.638-5.124-.015-14.485,11.231-15.437.033'%20fill='%231c63b7'/%3e%3cpath%20id='Path_29'%20data-name='Path%2029'%20d='M1.491,29.114c1.856-1.93,6.881-2.367,7.82.746.728,2.411-.643,4.012,2.813,4.974,3.982,1.109,13.614-2.852,11.658-7.077C21.585,23.011.212,23.607.968,12.884,1.682,2.752,23.406-2.952,31.2,1.569c5.617,3.257,2.7,10.441-2.3,8.826-1.39-.45-2.673-2.488-4.474-2.916-3.2-.761-7.713.289-10.6,1.8-2.546,1.333-5.255,3.421-1.655,5.466,5.217,2.964,18.467,4.162,19.606,11.19C34,39.626,13.023,46.447,3.445,39.368c-3.09-2.284-4.892-7.2-1.954-10.254'%20fill='%231c63b7'/%3e%3cpath%20id='Path_30'%20data-name='Path%2030'%20d='M113.607,4.54c7.281-1.322,8.492,7.916,1.851,8.817-6.284.853-7.853-7.727-1.851-8.817'%20fill='%231c63b7'/%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

New Mid-Term Management Plan(FY 3/2025 to FY 3/2027)

Since its "second founding" in 2020, Sanrio has been on a V-shaped recovery path and has continued to show robust growth.

In May 2023, as a "Value Creation Story we set a goal for the next 10 years of achieving 1 trillion yen in market capitalization and 50 billion yen in operating profit, and thanks to our fans and investors around the world who have loved and supported Sanrio, we were able to achieve these goals well in advance of schedule.

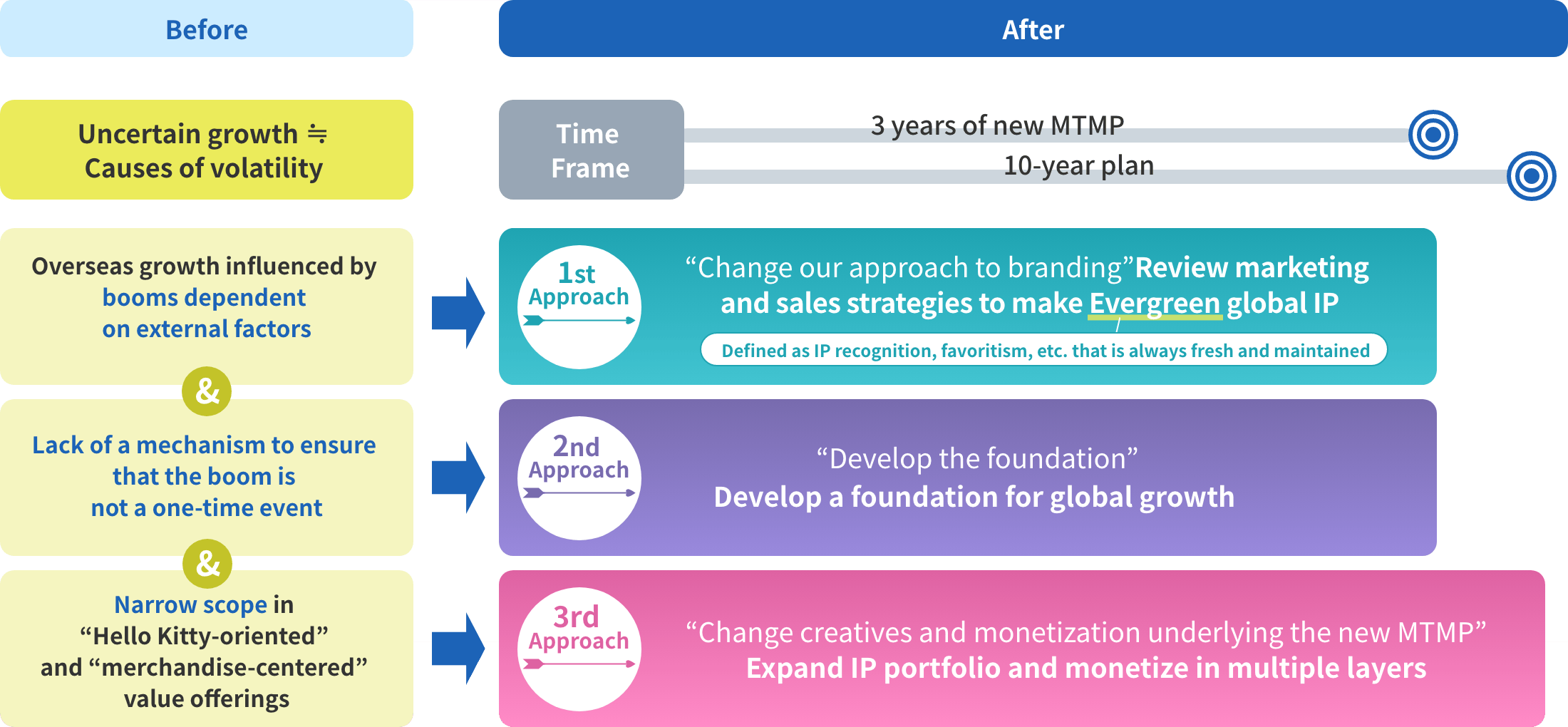

From uncertain growth to stable and perpetual growth based on “three approaches”

expand to full screen

New MTMP Targets

Aim for operating profit of 65 billion yen or more in the final year of the medium-term plan, and beyond that, aim for a 10-year average operating profit growth rate of 10% or more

Operating Profit Trend

expand to full screen

* Figures are before goodwill amortization in the case of a large-scale M&A.

Quantitative Targets and Financial Policy

We will further advance management from a cost-of-capital perspective to achieve market capitalization of 5 trillion JPY.

- Implementation Period

-

FY 3/2025 to FY 3/2027

- Quantitative targets

(FY3/2027) -

- Sales: 175 billion yen

- Operating Profit: over 65 billion yen

- Financial discipline*

(~ FY3/27) -

- Consider management that significantly exceeds the cost of capital, with a target ROE level of 30%

- Contribute to the strategy of the value creation story over the three-year cumulative period from FY03/2025 to FY3/2027

Consider organic investments (approx. 30 billion yen) and M&A and minority investments (50 billion yen and up) - Consider M&A targets with priority given to those that will maintain ROE at 30% level over the medium term even after acquisition

- Emphasizing not only dividends but also the expansion of TSR (Total Shareholder Return) through stock price appreciation.

- For large investments such as M&A, rigorous review will be conducted through the Investment Committee, and comprehensive decisions will be made based on both qualitative and quantitative aspects.

- Credit rating should be at the A-rated level. Goodwill/net asset ratio at the time of M&A should be within 70%, but it is acceptable for the rating to temporarily fall below the A-rated level.

- If funding becomes necessary in the future, we will consider fundraising options with a focus on capital cost, prioritizing them in the following order: bank senior loans and straight bonds > hybrid instruments (subordinated loans, subordinated bonds, etc.) > public equity offerings and convertible bonds.

- Shareholder returns

(medium to long term) -

- Dividend payout ratio of 30% or higher. In the absence of attractive investment opportunities, consider additional shareholder returns, taking into account surplus funds and financial strength (approx. 30 billion yen)

- Focus on increasing the total shareholder return due to higher share price, in addition to dividends

* In the event of a large-scale M&A, various indicators will be calculated based on operating profit, net profit, and EPS, with goodwill amortization added back.

Capital Allocation Policy (FY26-FY27)

Invest strategically with discipline and achieve stable shareholder returns

expand to full screen