Toward achieving a market capitalization of

5 trillion yen,

we are committed to management

conscious of cost of capital

Performance was driven by Hello Kitty’s 50th anniversary campaigns

Operating profit reaches record high for second consecutive year

In FY3/2025, sales increased 44.9% year-on-year to 144.9 billion yen, and operating profit rose 92.2% year-on-year to 51.8 billion yen, marking a record high for the second consecutive year. This strong performance was driven by initiatives to strengthen our global brand presence, centered around Hello Kitty’s 50th anniversary campaigns. The operating profit margin was 35.8%, and ROE was 48.6%, reflecting robust profitability and capital efficiency fueled by the expansion of the licensing business.

By region, North America led profit growth, driven by increased transactions with mass retailers. In Europe, apparel licensing performed well, particularly with fast fashion brands. In Asia, centered on Mainland China, growth was supported by both licensing operations and an expanded store network. In Japan, the product sales business benefited from strong inbound demand as well as a rise in domestic customer traffic, resulting in a broader customer base. The domestic licensing business also saw strong results, supported by Hello Kitty’s 50th anniversary campaigns and a targeted client strategy.

Updates to financial targets and policies and the aspirations embedded in our long-term vision

We have updated the financial targets and capital discipline policies of our medium-term management plan (FY3/2025–FY3/2027). Reflecting strong earnings growth in overseas markets—particularly in North America and Mainland China—we have raised the operating profit target for FY3/2027, the final year of the plan, from over 40 billion yen to over 65 billion yen.

As part of this update, we engaged in in-depth discussions on two key topics: first, whether to disclose a reference target for ROE; and second, our policy on shareholder returns in the event that no suitable M&A or minority investment opportunities—despite our active efforts—are identified.

Regarding the first topic, ROE is expected to decline from the exceptionally high level of 48.6% recorded in FY3/2025. This elevated ROE was driven by strong earnings growth centered on the highly capital-efficient licensing business, combined with a relatively low level of shareholders’ equity due to limited capital accumulation in past years. While maintaining a high ROE remains desirable, we plan to actively pursue M&A as part of our growth strategy. In the entertainment industry, M&A transactions often involve the recognition of substantial goodwill, which can result in a disproportionately high goodwill-to-net assets ratio. To mitigate this, we recognize the need to build up shareholders’ equity to a more appropriate level. Accordingly, we have set a reference target for ROE at 30%—a level we consider sufficiently high and sustainable while pursuing disciplined growth through M&A.

Regarding the second topic, we will continue to evaluate M&A and other investment opportunities through the Investment Committee, taking into account their strategic significance in light of our long-term vision, as well as their profitability, capital efficiency, and acquisition price. However, since such opportunities involve counterparties, there may be instances where we are unable to execute attractive investments. In such cases, considering our cash position, shareholders’ equity, and other relevant factors, we believe that additional shareholder returns would be appropriate from the perspective of capital efficiency.

We intend to manage our finances with a balanced approach, aligning our long-term ambitions with the expectations of our investors.

- Quantitative targets

(FY3/2027) -

- Sales: 175 billion yen

- Operating Profit: over 65 billion yen

- Financial discipline*

(~ FY3/27) -

- Consider management that significantly exceeds the cost of capital, with a target ROE level of 30%

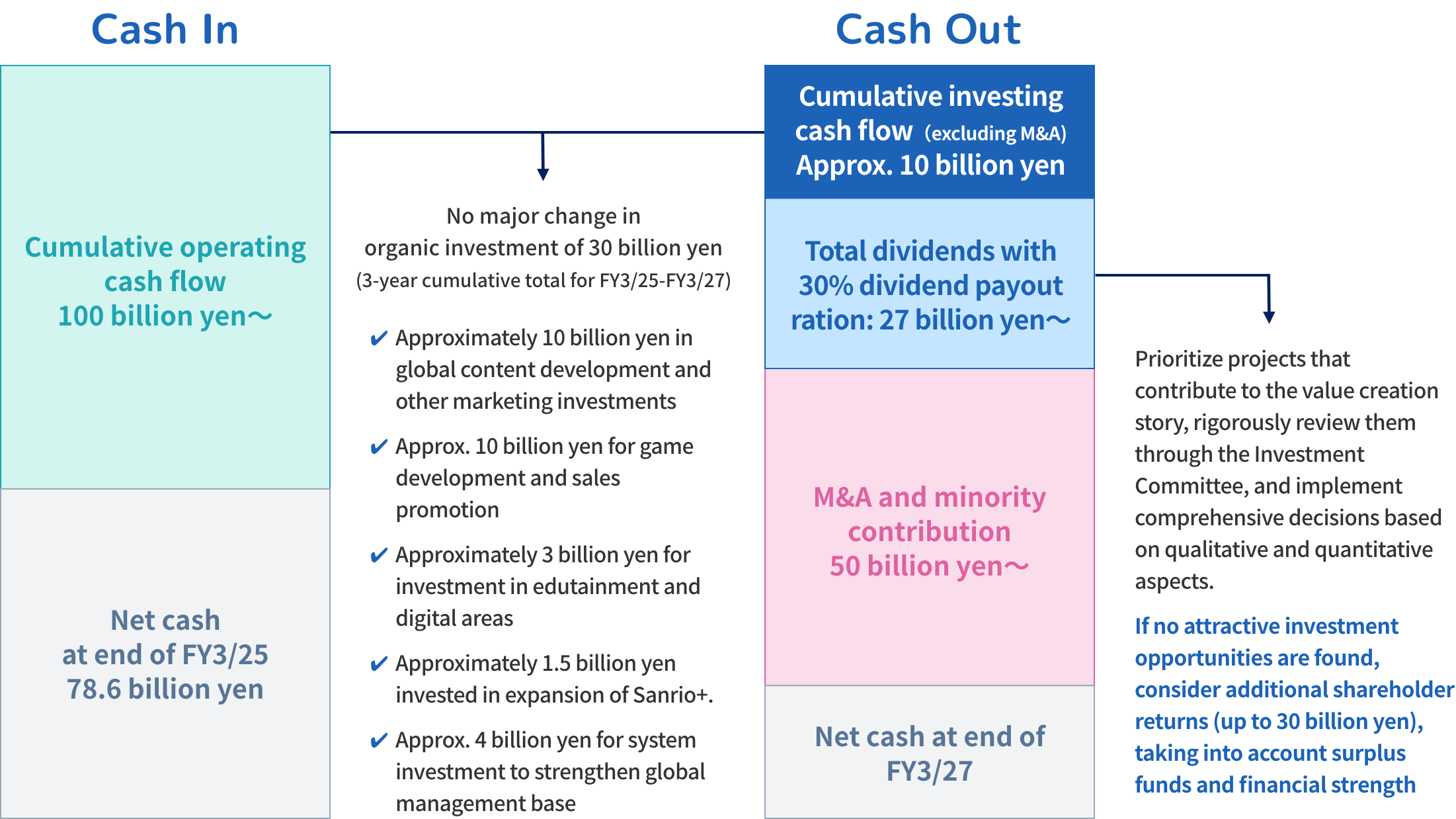

- Contribute to the strategy of the value creation story over the three-year cumulative period from FY03/2025 to FY3/2027

Consider organic investments (approx. 30 billion yen) and M&A and minority investments (50 billion yen and up) - Consider M&A targets with priority given to those that will maintain ROE at 30% level over the medium term even after acquisition

- Emphasizing not only dividends but also the expansion of TSR (Total Shareholder Return) through stock price appreciation.

- For large investments such as M&A, rigorous review will be conducted through the Investment Committee, and comprehensive decisions will be made based on both qualitative and quantitative aspects.

- Credit rating should be at the A-rated level. Goodwill/net asset ratio at the time of M&A should be within 70%, but it is acceptable for the rating to temporarily fall below the A-rated level.

- If funding becomes necessary in the future, we will consider fundraising options with a focus on capital cost, prioritizing them in the following order: bank senior loans and straight bonds > hybrid instruments (subordinated loans, subordinated bonds, etc.) > public equity offerings and convertible bonds.

- * In the event of a large-scale M&A, various indicators will be calculated based on operating profit, net profit, and EPS, with goodwill amortization added back.

As part of our long-term vision through FY3/2035, we aim to achieve a market capitalization of 5 trillion yen and deliver a 10-year CAGR of 10% or higher in operating profit. We understand that market capitalization is shaped by a range of factors—including profitability, capital efficiency, and future growth expectations—as assessed by the market. Our goal is not simply to grow sales or profit, but to maximize corporate value by steadily executing the strategies set forth in our value creation story. We hope shareholders and other stakeholders will understand and support this vision.

The majority of our sales will continue to be generated by the highly profitable licensing business, and we aim to maintain strong profitability and capital efficiency even 10 years from now. We have intentionally not disclosed a specific operating profit target, as our primary message is the importance of reducing volatility and our commitment to stable growth.

We set a 10-year target for operating profit CAGR of 10% or higher, based on investor feedback indicating that Sanrio’s stock price tends to decline when growth falls below double digits. With this target, we aim to clearly convey our commitment to sustaining a high growth rate—of at least double digits, even at a minimum.

Capital allocation with a balanced focus on investment and shareholder returns

Since making a major investment in the 1990s to launch our theme park, we have not undertaken any large-scale investments. Under the current medium-term management plan, however, we have allocated 30 billion yen for organic investment and over 50 billion yen for M&A and related activities, marking a shift into a full-scale investment phase. To ensure that these investments contribute to enhancing corporate value, we have established an Investment Committee. With input from external advisors, we have defined clear investment criteria and key considerations for each category—M&A, minority stakes, existing businesses, and new ventures. All investment decisions will be made based on an objective framework.

In FY3/2025, the Investment Committee convened 16 times, primarily to review proposals related to game development and M&A. Each proposal was thoroughly examined from multiple perspectives by both internal and external committee members, with in-depth discussions on factors such as strategic relevance and expected financial returns. Some potential M&A deals were substantial in scale; however, many were ultimately declined due to valuation gaps or risk factors identified during the due diligence process, which made it unlikely that they would deliver appropriate returns. We will continue to actively evaluate a wide range of investment opportunities while maintaining disciplined decision-making based on strict investment criteria.

Regarding capital allocation, we aim to strike a balance between strategic investment and shareholder returns. During periods of strong performance, we generate solid operating cash flow, and by maintaining a dividend payout ratio of around 30%, we expect to retain ample free cash flow. Under the current medium-term management plan, we have allocated over 50 billion yen for M&A. However, if we do not identify attractive opportunities, we will consider reallocating up to an additional 30 billion yen to shareholder returns.

Regarding capital allocation, we aim to strike a balance between strategic investment and shareholder returns. Under the current medium-term management plan, we have allocated 30 billion yen for organic investment and over 50 billion yen for M&A and related activities, signaling a transition into a full-scale investment phase for the Company.

expand to full screen

Achieved 1 trillion-yen market cap significantly ahead of schedule

We place great importance on our share price. In May 2023, we set a 10-year target of achieving a market capitalization of 1 trillion yen. Thanks to the support of fans and investors around the world, we reached this goal significantly ahead of schedule—in October 2024.

In December 2024, strategically held shares owned by a megabank were sold to global institutional investors and domestic retail investors through a global offering. Leading up to the offering, we devoted significant time to refining our equity story to clearly communicate our strengths, and to designing an optimal structure aimed at realizing our desired shareholder composition. Following the announcement, we conducted an efficient online roadshow, arranging meetings with investors around the world and striving to address each of their questions with care. As a result, the offering was highly regarded and was named the 2024 Equity Deal of the Year by Deal Watch.

The number of IR meetings increased from 336 in FY3/2024 to 412 in FY3/2025. The number of companies we met with, including duplicates, also rose from 680 to 1,163 over the same period.

Our next target is to reach a market capitalization of 5 trillion yen by FY3/2035. While the most direct path to achieving this goal is the steady execution of the initiatives outlined in our long-term vision, we also place importance on the following investor relations priorities.

First, we consider dialogue with investors and analysts a top priority. While the IR team serves as the primary point of contact, we proactively create opportunities for direct engagement with the President, myself, and other members of the Board. Feedback from these interactions is promptly shared with the management team and outside directors and is actively reflected in future management decisions.

Second, we are committed to enhancing the visibility and transparency of our disclosures. We believe that timely and sincere communication is essential to achieving a fair market valuation. In addition to quarterly earnings briefings, we will continue to hold small-group meetings with sell-side analysts, participate in various events, and engage with individual investors. When we receive requests for specific events or additional disclosures on particular topics, we will make every effort to accommodate them wherever possible.

Through these initiatives, we aim to pursue management that is conscious of the cost of capital, with the goal of achieving a market capitalization of 5 trillion yen.